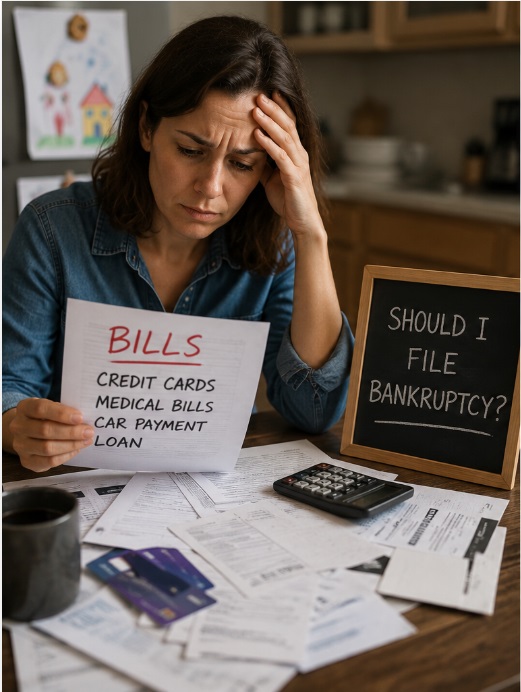

Thinking About Bankruptcy? Do Not Let Fear Make the Decision for You

For many people, bankruptcy becomes a consideration only after years of financial strain. They may rely on credit cards for ordinary living expenses, make minimum payments that barely reduce their balances, borrow from relatives, or withdraw retirement savings simply to remain current.

For many people, bankruptcy becomes a consideration only after years of financial strain. They may rely on credit cards for ordinary living expenses, make minimum payments that barely reduce their balances, borrow from relatives, or withdraw retirement savings simply to remain current.

Bankruptcy does not provide the right solution in every situation. It can affect property, credit, taxes, pending litigation, co-signers, and future financial choices. But many people reject bankruptcy because they rely on overstated fears or incomplete information.

These are three of the most misunderstood reasons people choose not to file bankruptcy.

1. “I Cannot File Bankruptcy Because It Will Ruin My Credit.”

A bankruptcy filing can affect credit and become part of the public court record. Those concerns deserve serious consideration.

However, many people considering bankruptcy already have substantial credit damage. Late payments, high credit-card utilization, collection accounts, judgments, repossessions, and foreclosure activity may already harm their credit history. Continued unaffordable payments do not necessarily preserve credit or improve long-term financial stability.

The more important question is not simply whether bankruptcy will affect a credit score. The question is whether debt payments prevent someone from paying essential expenses, maintaining insurance, building emergency savings, or protecting a home and family.

A Chapter 7 discharge can eliminate personal liability for many unsecured debts, including credit-card balances, medical bills, personal loans, repossession deficiencies, and collection accounts. When the bankruptcy court enters a discharge, creditors generally cannot continue collecting discharged debts. Some debts may survive bankruptcy, including many taxes, domestic-support obligations, certain student loans unless the debtor takes additional steps to remove or reduce them, and debts arising from fraud or intentional misconduct. See 11 U.S.C. §§ 523 and 524.

Credit should play one part in a broader financial analysis. It should not become the sole reason someone sacrifices financial security to make payments they cannot realistically sustain.

2. “I Cannot File Bankruptcy Because I Will Lose My Home, Car, or Everything Else.”

This concern remains one of the most persistent myths about bankruptcy.

A Chapter 7 trustee may sell property that exemptions do not protect. Before filing, a person needs a careful review of assets, liens, income, transfers, and available exemptions.

But bankruptcy does not automatically require someone to lose a home, vehicle, or personal belongings.

Exemption laws protect certain categories of property from creditors. In Arizona, those protections may cover a residence, household goods, vehicles, retirement accounts, wages, and other property, depending on the facts and applicable law. Arizona adjusts its homestead exemption annually for inflation. In bankruptcy, the law generally determines the available exemption as of the petition date. Equity, liens, ownership interests, recent refinancing, transfers, and the type of property can all affect the analysis. See A.R.S. § 33-1101.

Many Chapter 7 cases qualify as “no-asset” cases. In those cases, the trustee does not sell property for unsecured creditors because exemptions protect the property, valid liens fully secure it, or its value offers no meaningful benefit to the bankruptcy estate.

A homeowner who has fallen behind on mortgage payments may have options under Chapter 13. In appropriate circumstances, Chapter 13 can stop a foreclosure sale and allow the homeowner to repay mortgage arrears over time while continuing regular mortgage payments. Timing, income, feasibility, and the status of any foreclosure sale determine whether Chapter 13 can help.

Do not assume bankruptcy will cause you to lose everything. Do not assume you will keep everything either. Your individual facts determine the answer.

3. “I Should Keep Paying Until I Have Absolutely No Other Choice.”

Many people believe they should consider bankruptcy only after exhausting every financial resource. They may withdraw retirement funds, borrow against home equity, sell protected assets, borrow from family, postpone medical care, or use one credit card to pay another.

That strategy can make a difficult financial situation substantially worse.

Before withdrawing protected retirement funds, borrowing against a home, selling exempt property, transferring assets, or taking out a high-interest loan, understand the possible consequences. Some actions can reduce protections otherwise available in bankruptcy. Transfers to family members, unusually large payments to certain creditors, and new borrowing shortly before filing may create significant issues that require full disclosure and could open you or others to challenges by the trustee and/or your creditors.

Bankruptcy law requires complete honesty. A debtor must disclose assets, debts, income, expenses, transfers, and other financial information. Anyone who hides property, secretly repays family members, or omits information from bankruptcy documents may face serious legal consequences.

Federal bankruptcy law does not punish people who experience financial difficulty. It gives honest individuals a structured legal process for addressing debt when repayment no longer makes financial sense.

Sometimes waiting makes sense. A person may need time to resolve litigation, complete a real-estate transaction, determine tax obligations, or decide whether Chapter 7 or Chapter 13 offers the better solution. But delaying because of guilt, fear, or misinformation can deplete savings and lead to additional interest, lawsuits, wage garnishments, repossessions, or foreclosure.

Bankruptcy Is a Financial Decision—Not a Moral Failure

People often feel ashamed when they cannot pay every debt. Financial distress can arise from job loss, illness, divorce, reduced income, business failure, caregiving responsibilities, inflation, or unexpected emergencies.

People often feel ashamed when they cannot pay every debt. Financial distress can arise from job loss, illness, divorce, reduced income, business failure, caregiving responsibilities, inflation, or unexpected emergencies.

People should base the decision to file bankruptcy on accurate financial and legal information, not fear or embarrassment.

Before deciding whether bankruptcy makes sense, review:

- Household income and reasonable living expenses.

- Secured and unsecured debts.

- Home equity, vehicles, retirement accounts, and other assets.

- Lawsuits, garnishments, repossessions, and foreclosure deadlines.

- Taxes, student loans, child support, criminal fines, and other obligations that may not be discharged.

- Recent transfers, refinancing, large payments, cash advances, or loans from relatives.

An experienced bankruptcy attorney, who cares more about you and not how much money they can make, can assess whether filing now, filing later, pursuing Chapter 7, or Chapter 13, or choosing another option best serves your circumstances.

The Bottom Line

The three most misunderstood reasons not to file bankruptcy involve fear of credit damage, fear of losing everything, and the belief that a person must sacrifice every possible resource before seeking help.

Those concerns deserve serious attention. But people should evaluate them based on actual facts, applicable law, and their long-term financial position—not on myths.

Bankruptcy may not provide the right answer in every case. Yet accurate advice before financial problems intensify may preserve more options, more property, and greater peace of mind.

Link to YouTube video – Three Misunderstood Reasons People Decide Not to File Bankruptcy

Diane is a well respected Arizona bankruptcy and foreclosure attorney. As a retired law professor, she believes in offering everyone, not just her clients, advice about bankruptcy and Arizona foreclosure laws. Diane is also a mentor to hundreds of Arizona attorneys.

*Important Note from Diane: Everything on this web site is offered for educational purposes only and not intended to provide legal advice, nor create an attorney client relationship between you, me, or the author of any article. Information in this web site should not be used as a substitute for competent legal advice from an attorney familiar with your personal circumstances and licensed to practice law in your state. Make sure to check out their reviews.*

In Case You Missed It

Published On: June 27, 2026

Merchant cash advances can provide fast cash, but daily withdrawals, stacked MCA loans, SBA loan conflicts, personal guarantees, and bankruptcy risks can quickly put a business and its owner in danger.

Published On: June 26, 2026

Bankruptcy Is Not Just Paperwork: Some Simple Mistakes That Can Cost You For many people, bankruptcy is not the first choice. It is usually something they consider only after they have done everything they know [...]

Published On: June 24, 2026

Build Financial Stability, Not Just a Better Credit Score A good credit score can be helpful. It may make it easier to rent an apartment, obtain a mortgage, finance a vehicle, or qualify for lower [...]

Published On: June 13, 2026

Worried about losing your tax refund when you file bankruptcy in Arizona? Arizona law may protect the part of your refund that comes from the Earned Income Tax Credit and Child Tax Credit. Learn what may be protected, what a trustee may claim, and why timing matters before you file.