COLLECTION LETTERS & TELEPHONE CALLS

At one time, all of us have been contacted by a bill collector.

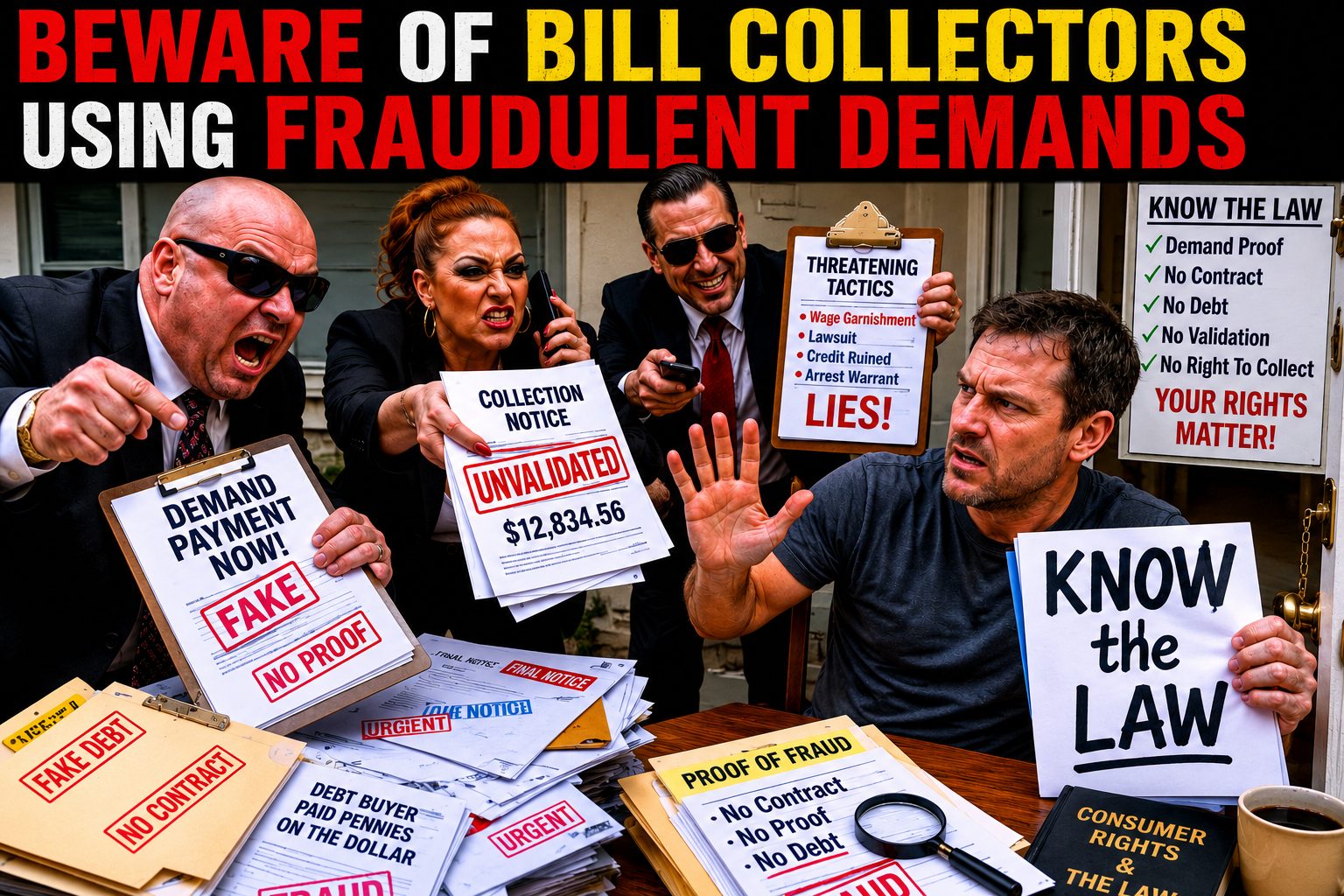

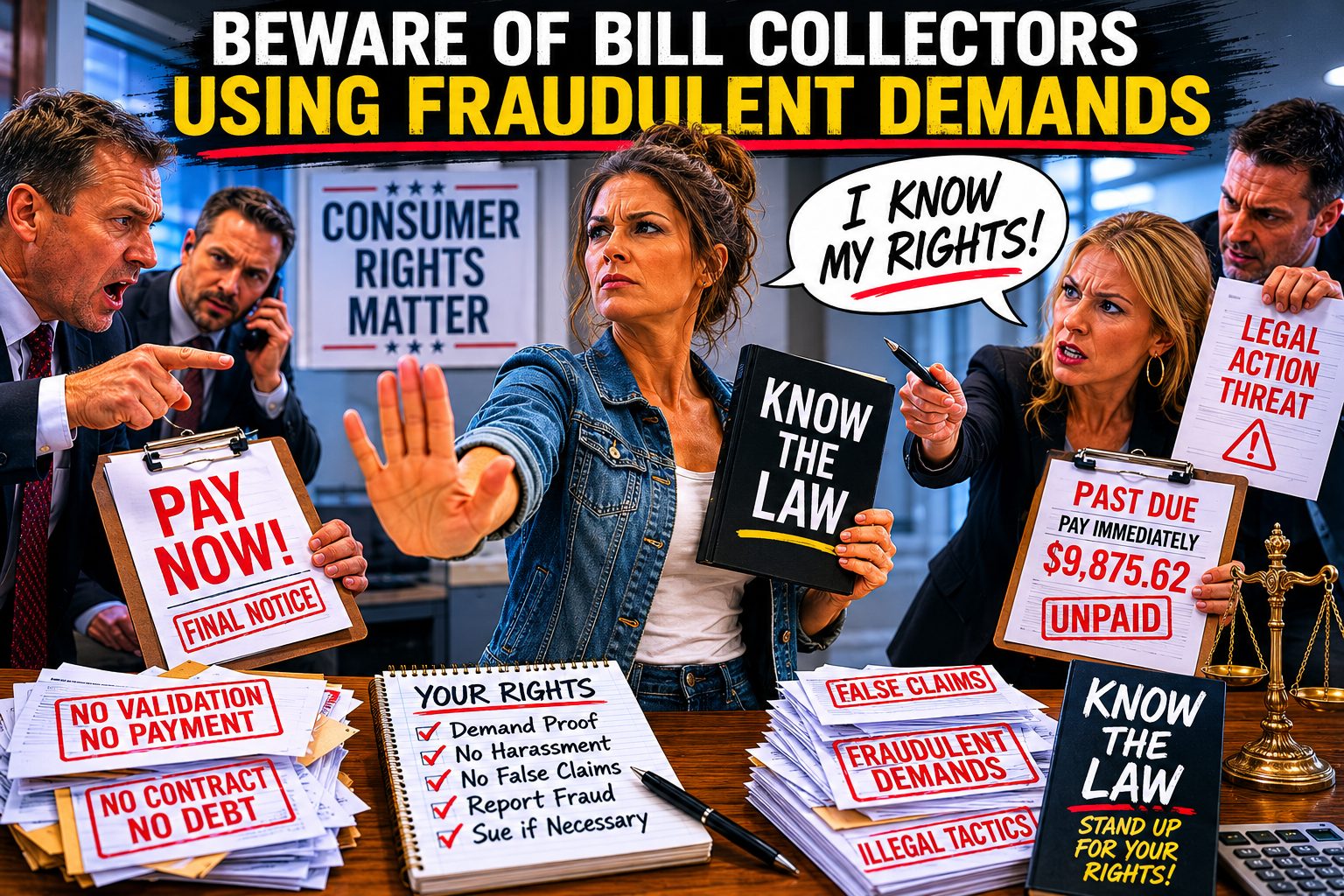

We forget to pay or fall behind on payments on credit cards, mortgages, cars, medical bills, or other situations involving bills. Then, we get a letter or telephone call. For some these calls can become a terror attack by their creditors. The creditors are calling at all hours at home and work. They are calling the neighbors, the family and employers. They are obnoxious, condescending and downright rude when you do talk to them. Despite the laws governing their actions many creditors and collection companies feel that an individual will not have the time, money or emotional strength to pursue them in court. Therefore, they get away with the outrageous and, sometimes, illegal acts.

We forget to pay or fall behind on payments on credit cards, mortgages, cars, medical bills, or other situations involving bills. Then, we get a letter or telephone call. For some these calls can become a terror attack by their creditors. The creditors are calling at all hours at home and work. They are calling the neighbors, the family and employers. They are obnoxious, condescending and downright rude when you do talk to them. Despite the laws governing their actions many creditors and collection companies feel that an individual will not have the time, money or emotional strength to pursue them in court. Therefore, they get away with the outrageous and, sometimes, illegal acts.

If you have filed bankruptcy, it is contempt of a federal restraining order (called the automatic stay) for the creditor or his collection company to contact you.

If your case is still open 11 U.S.C. Section 362 prohibits this contact without permission of the Bankruptcy Court. If your case is discharged then creditors and their collection companies are permanently enjoined from contacting you unless they have received special permission from the Bankruptcy Court, or your debt is one that is excepted from your discharge.

If your case is still open 11 U.S.C. Section 362 prohibits this contact without permission of the Bankruptcy Court. If your case is discharged then creditors and their collection companies are permanently enjoined from contacting you unless they have received special permission from the Bankruptcy Court, or your debt is one that is excepted from your discharge.

Whether the collectors call themselves credit representatives, account supervisors, or collection agents, the bill collector’s job is to get money out of your pocket and put it into his or hers. These collectors normally are paid about 25% of whatever money they bully you into paying. They will not look at your account to see if the bill is correct, at least not in the initial stages of collection. The collectors or agents accept what the computer tells them.

Many of these collectors admit they do not have access to the account records and “really don’t care if the records are accurate.”

The collection letters that you receive are usually computer-generated and often do not have a signature on them. The collectors often threaten to report you to credit reporting agencies, which could ruin your credit, or they threaten to sue you for the amount they claim you owe. Most of the calls come from outside the United States. They don’t care about the truth, the collector only wants their commission.

The collection letters that you receive are usually computer-generated and often do not have a signature on them. The collectors often threaten to report you to credit reporting agencies, which could ruin your credit, or they threaten to sue you for the amount they claim you owe. Most of the calls come from outside the United States. They don’t care about the truth, the collector only wants their commission.

Perhaps the most annoying tactic, used by bill collectors, is constant telephone calls demanding money.

The phone calls arrive at inconvenient times and places. The collectors often call at work and embarrass you in front of your co-workers. Often the collector has an obnoxious attitude and manner, acting like you are somehow a criminal.

THE GOOD NEWS IS…

You have legal rights that protect you against all of the above practices.

Let’s begin by describing what you should do when you start getting bills. If you feel you owe no money or the bill collector’s amount is incorrect, write a letter to both the collection company and the original creditor stating you owe no money or the amount owed is incorrect. You should also ask for a record of your payments.

Let’s begin by describing what you should do when you start getting bills. If you feel you owe no money or the bill collector’s amount is incorrect, write a letter to both the collection company and the original creditor stating you owe no money or the amount owed is incorrect. You should also ask for a record of your payments.

Disputing a bill

If the bill collectors report the debt to a credit reporting agency, you should write to the credit reporting agency and tell them the bill is in dispute. Whenever you write to a bill collector or to the reporting agency, you should sign the letter, date it, and keep a copy for your file. Remember, just calling the bill collector to say you do not owe the money may not leave a permanent record of the call. Like most bureaucracies, if it is not in writing, it does not exist.

STOP ANNOYING TACTICS

If the collectors continue to call you, you can send them a letter (sample below) requesting they cease communication with you under the terms of the Fair Credit Collection Practices Act, 15 U.S.C.S. Section 1692.

When you write your letter, do not forget to date it, sign it, and keep a copy. If you would like them to pay attention, consider sending the letter CERTIFIED. By sending the letter CERTIFIED, you have proof that you sent it. If you send this letter, it will not only stop letters from being sent to you, but it will also stop telephone calls from being made to you.

When you write your letter, do not forget to date it, sign it, and keep a copy. If you would like them to pay attention, consider sending the letter CERTIFIED. By sending the letter CERTIFIED, you have proof that you sent it. If you send this letter, it will not only stop letters from being sent to you, but it will also stop telephone calls from being made to you.

Telephone calls from bill collectors are one of the most annoying, draining, embarrassing and demoralizing experiences anyone can encounter. The bill collectors count on these bullying tactics to work because you pay them. Perhaps you pay them with funds that should be used to pay your mortgage, car or food for your family. Many of their actions are illegal and they know it. The bill collectors don’t care, they know that they get paid a large percentage of the funds that they bully you into paying. They assume you do not know your rights and will not report them to the proper authorities.

Collection Practices Act), forbids bill collectors from calling you at inconvenient times, such as before 8:00 a.m. or after 9:00 p.m.

T he collectors or agents cannot communicate with third parties such as your neighbor, your friend, or your great aunt Matilda. They cannot contact you at work if they know (notice must be in writing) that your employer prohibits it. They cannot threaten you with criminal prosecution or call you on the phone repeatedly with the intention of harassing you.

he collectors or agents cannot communicate with third parties such as your neighbor, your friend, or your great aunt Matilda. They cannot contact you at work if they know (notice must be in writing) that your employer prohibits it. They cannot threaten you with criminal prosecution or call you on the phone repeatedly with the intention of harassing you.

Debt collectors cannot use any false, deceptive, or misleading representation by any means in connection with the collection of your debt.

Here is the law (that does not mean they don’t break the law): They cannot use or threaten violence. They cannot use obscene or profane language. They cannot claim you will be imprisoned or your property seized unless they are the lender. They cannot pretend to be an attorney or add fees/charges that are not authorized. Also, the collectors cannot pretend to be someone else just to get in touch with you. They cannot threaten to take any action that cannot legally be taken or that they do not intend to take; they cannot take a postdated check and then deposit it before the date on the check.

All of the above is contained in the Fair Credit Collection Practices Act, 15 U.S.C.S. Section 1692. If a bill collector violates any of the provisions of the Act, he/she can be sued in court. The credit agency can also be reported to the State of Arizona, which regulates credit collection agencies located within Arizona. This law does not apply to the original creditor.

If a bill collector comes to your house, it is your choice whether to talk to him or not.

If you do not wish to speak with him, inform him that he is trespassing and call the police. If a repo agent comes to your house, your car is parked on private property (not in the street) and you do not want him to take your vehicle, you should tell him you refuse to give him permission for repossession and he must leave immediately because he is trespassing. If the repo agent or agents refuse to leave, call the police. If you live on any of the Indian Reservations, you do not have to turn your car or mobile home over to a repossession agent. On the Reservation, repossessions can only be done voluntarily (in other words, if the car owner gives the repossession agent permission to take the car, then the car is given on a voluntary repossession). If you do not give permission for the agent to take the car, the agent must go to the tribal court, sue the owner of the car for repossession, and get an order from the tribal court for repossession of the vehicle.

If you do not wish to speak with him, inform him that he is trespassing and call the police. If a repo agent comes to your house, your car is parked on private property (not in the street) and you do not want him to take your vehicle, you should tell him you refuse to give him permission for repossession and he must leave immediately because he is trespassing. If the repo agent or agents refuse to leave, call the police. If you live on any of the Indian Reservations, you do not have to turn your car or mobile home over to a repossession agent. On the Reservation, repossessions can only be done voluntarily (in other words, if the car owner gives the repossession agent permission to take the car, then the car is given on a voluntary repossession). If you do not give permission for the agent to take the car, the agent must go to the tribal court, sue the owner of the car for repossession, and get an order from the tribal court for repossession of the vehicle.

Document all your discussions and communications with any debt collectors.

If the collection company is taking illegal actions then get as much proof as possible – log all calls, record all discussions (if you state permits it), put them on speaker phone and have a third party witness the discussion. If they cross the line, then file a complaint with the Arizona Department of Financial Institutions and the Federal Trade Commission. Include copies of your written notes and demands. Make sure you send a copy of the complaint(s) to the offending company and the original creditor.

If the collection company continues to ignore your warnings and refuses to comply with the law then you could sue them.

But their behavior must be truly offensive, not just annoying. You could bring an action in small claims court, or hire a lawyer. But, you must have proof of their actions in order for any court to find in your favor. In order to have this proof you need to keep a diary of all calls, the time and date, what was said and whether or not you told them to stop calling.

SAMPLE LETTER TO CREDITORS OR COLLECTION COMPANIES:

CERTIFIED, RETURN RECEIPT REQUESTED

Date:

(Creditor’s Name and Address)

RE: Account Number

Debtor’s Name

Dear (Name of Collection Agency Representative):

This letter is intended to notify you the cease all communication with me, any member of my family, relatives, neighbors or employers pursuant to 15 U.S.C. Section 1692(c), Federal Debt Collection Practices Act, Section 805(c).

You may notify me in writing of your intention to terminate collection or of your intention to pursue specific remedies.

This written notice to cease communication shall not be construed as an admission with respect to the above mentioned account.

Sincerely,

(Your name)

NOTE: it is very important that you keep of copy of this communication for your records

If you wish, you may want to write a few lines explaining your situation at the bottom of the page. For example, you may want to state your age, and/or the fact that you are disabled and therefore unable to work. If you are living on Social Security and have no other income, you may want to put that in your note. Also, you may want to state that you want to pay the bills you owe, but simply cannot afford to pay them at this time. You are not required to give any reason why you cannot or will not pay the alleged debt, but it could be to your benefit. For example, the collection agent may decide to focus collection efforts on others who have a greater ability to pay.

MAKE THREE COPIES OF THE LETTER

Send the original to the collection agency; a copy to the creditor; and a copy to (this address may be outdated so check the FTC website):

Southeast Region

Federal Trade Commission

Suite 1500

225 Peachtree Street, NE

Atlanta, GA 30303

Send these letters certified mail, return receipt requested. Keep the third copy of the letter, the Certified Mail receipts, and the green cards (which you should receive back in the mail) for your records.

The collection agency should then stop contacting you except to provide information about their basis for claiming that you owe a debt. If they continue to contact you, file a complaint to Federal Trade Commission and Consumer Financial Protection Bureau.