This website is not intended to be a legal advice resource. It is only meant to be used for educational reasons. Please don’t take any action or refrain from taking any action based on what you’ve read on this website. This website, article, or link may contain outdated, incorrect, or irrelevant information. It is your obligation to speak with an expert attorney who can apply current legislation or laws to your personal situation in a professional manner.

This website is not intended to be a legal advice resource. It is only meant to be used for educational reasons. Please don’t take any action or refrain from taking any action based on what you’ve read on this website. This website, article, or link may contain outdated, incorrect, or irrelevant information. It is your obligation to speak with an expert attorney who can apply current legislation or laws to your personal situation in a professional manner.

There is no attorney-client relationship formed by using this site or communicating with Law Office of D.L. Drain or any of our employees. Please read the complete disclaimer for additional information.

It is vital that you seek legal advice from a qualified attorney on your individual situation. It will almost certainly cost you less to seek advice before acting than it will to repair your mistakes.

PROOF OF CLAIM

IMPORTANT: THIS FIRM MAKES NO REPRESENTATIONS AS TO THE ACCURACY OR CURRENT STATUS OF ANY LAW, CASE, ARTICLE OR PUBLICATION CITED HEREIN OR LINKED TO. WARNING – SOME OF THESE REFERENCES ARE PRE-BAPCPA.

Excerpt from Insolvency Insights, By Paul Hammer

DON’T BE LATE – FILING PROOFS OF CLAIMS IN A BANKRUPTCY CASE

When a creditor is notified that a debtor has filed for bankruptcy, the creditor should be careful to determine whether it needs to file a Proof of Claim in the case to preserve its rights to receive payments from the bankrupt estate. This article goes over the importance of a creditor acting in a timely and proper fashion and preserving its rights in the bankruptcy process.

Cases Under Chapter 7 and 13

In these types of cases, the creditor will not share in any distribution of funds from the bankruptcy estate unless it has filed a timely Proof of Claim. Cases that are originally filed under Chapters 11 and 13, but are later converted to Chapter 7, are subject to the setting of a new bar date, i.e. the deadline for the filing of claims, which will be a reasonable amount of time (usually around 90 days) after the celebration of the creditor’s meeting with the newly assigned liquidation Trustee.

Cases Under Chapter 11 – Important Difference

In these types cases, a very important wrinkle is added that creditors need to be on the lookout for. Generally, is not necessary to file a claim if the creditor agrees with the amount the debtor has listed as due in its Schedules and the debtor has not listed the debt as disputed, contingent or unliquidated. However, if the creditor believes it is owed more money than indicated by the debtor, or its claim is listed as disputed, contingent or unliquidated, the creditor must file a claim for the full amount owed, or risk losing all of its rights as to the subject debt.

Effective December 1, 2017: Certain amendments to the Bankruptcy Rules will become effective. Below are two of the changes: 1) The period for filing proofs of claim is shortened, and 2) secured creditors must timely file a claim to receive a distribution.

Effective December 1, 2017: Certain amendments to the Bankruptcy Rules will become effective. Below are two of the changes: 1) The period for filing proofs of claim is shortened, and 2) secured creditors must timely file a claim to receive a distribution.

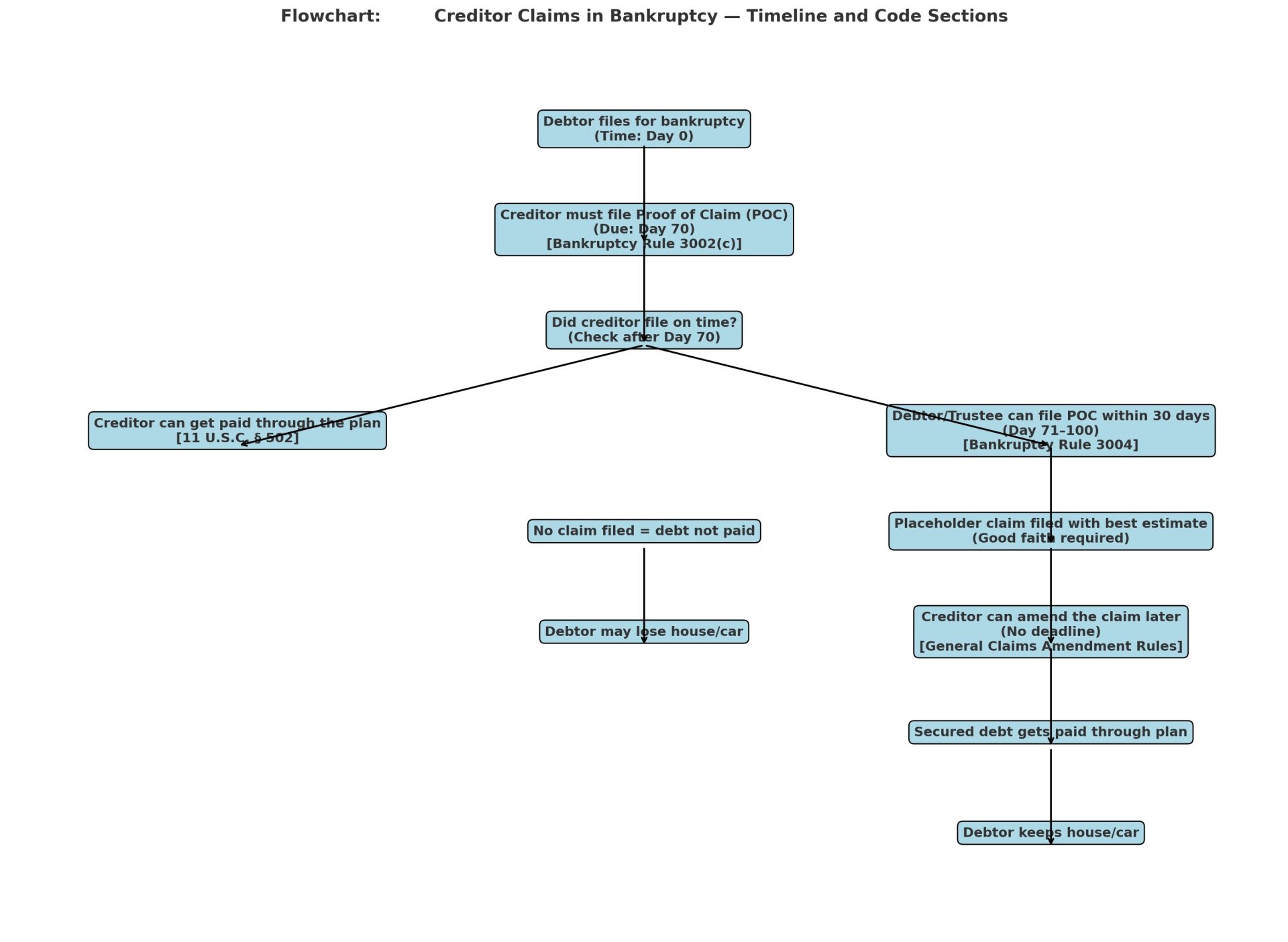

Most bankruptcy proceedings now have a shorter time period for filing proofs of claim. Under the amendment to Rule 3002(c) of the Bankruptcy Rules, the deadline for filing a proof of claim in voluntary cases under Chapters 7, 12, and 13 is now 70 days after the bankruptcy is filed, or if converted to 7 or 13, then from the date of conversion. Governmental units can file claims up to 180 days following the relief order.

Extension of deadline: Courts may grant an extension of the filing deadline based on a motion filed under amended Rule 3002(c)(6)(A), if the creditor did not receive notice in time to file a timely proof of claim because the debtor failed to timely file the list of creditors’ names and addresses required by Rule 1007(a). If the court grants such a motion for extension, the extension may be no more than sixty days from the date of the order granting the motion.

The second change affects secured creditors. Under the newly amended Rule 3002(a), secured creditors will be required to file a claim by the claims bar date to receive a distribution from the debtor’s estate. The new Rule 3002(a) also clarifies, in accordance with Section 506(d) of the Bankruptcy Code, that the failure to file a proof of claim does not affect the lien securing the debt. As a result, whether or not the secured creditor files a claim will not disturb the creditor’s lien rights.

Holders of claims secured by a security interest in the debtor’s principal residence are given additional time to file supplemental attachments to the proof of claim. Rule 3002(c)(7)(B) provides that any attachments required by Rule 3001(c)(1) and (d), such as a copy of the mortgage or deed of trust and evidence that the security interest is perfected, must be filed as a supplement to the holder’s claim not later than 120 days after the petition date.

The following are pre-December 1, 2017 cases:

On a question where the courts are divided, Bankruptcy Judge Mary Ann Whipple of Toledo, Ohio, took sides with the Seventh Circuit and held that the claim filing deadline in Bankruptcy Rule 3002(c) applies to secured creditors in chapter 13 cases, even though secured creditors are not required to file claims in chapter 13 cases.

In chapters 7 and 13, secured creditors are not required to file claims. After bankruptcy, they may enforce their liens against the debtor’s property, although they would have waived any unsecured deficiency claims and retained no claims against the debtor personally. Secured creditors will often refrain from filing claims to avoid submitting to the jurisdiction of the bankruptcy court and the possibility of having consented to entry of a final order in bankruptcy court.

In In re Pajian, 785 F.3d 1161 (7th Cir. 2015), the bankruptcy judge believed that a secured creditor could file a claim in a chapter 13 case at any time before confirmation. On direct appeal, the Seventh Circuit reversed in May 2015, holding that secured creditors must file claims in chapter 13 cases by the same deadline that applies to unsecured creditors.

In re Dumbuya, 15-33176 (Bankr. N.D. Ohio Feb. 6, 2017) Judge was persuaded by the Seventh Circuit’s conclusion that “principles of sound judicial administration” call for making the deadline applicable to secured claims, otherwise a secured creditor could “swoop in at the last minute and upend a carefully constructed payment schedule.”

December 1, 2011 (NOTE SEE NEW RULE CHANGES): rule changes related to proofs of claim: Pursuant to Rule 3001(c), proofs of claim must be made in writing. Official Form B-10 is the proof of claim form. Official Form B-10 has changed and the instructions for completing the proof of claim have changed. Creditors must now include information about the interest rate, each creditor must now sign off on a statement that it has attached documentation that is evidence of the creditor’s perfected security interest, and the signature block of Official Form B-10 has changed.

Rule 3001(c)(2) has been amended and is now entitled “Additional Requirements in an Individual Debtor Case; Sanctions for Failure to Comply”. The changes require a claimant to include an itemized statement of the prepetition interest, fees, expenses or charges with a proof of claim, as well as a statement of the amount necessary to cure a default as of the petition date. If the mortgage payments include an escrow payment, an escrow statement must also be attached to the proof of claim. These requirements can be partially fulfilled by the completion and filing of new Official Form B10, Attachment A.

To complete Official Form B10, Attachment A, Part 1, the mortgage creditor must itemize the amount of principal and interest due as of the date of the filing of the bankruptcy petition, and the total interest due as of the petition date must be broken down by interest rate and the corresponding time periods. Part 2 requires a description of the fees, expenses and charges incurred in connection with the claim, as of the petition date, the dates these charges were incurred and the amounts of these charges.

Part 3 requires a statement of the amount necessary to cure the default as of the petition date. It is in this section that a mortgage creditor will check off the box indicating whether or not the mortgage payments that are in arrears include an escrow component. If so, the mortgage creditor must include a copy of an escrow statement. Also required in Part 3 is the date the last payment was received by the creditor, the number of payments due, and the amount of the payments due which the mortgage creditor must further analyze by adding the total of prepetition fees and expenses to the overdue payments and subtracting the total of any unapplied funds, resulting in an amount which is the total amount necessary to cure the default as of the petition date.

The bankruptcy court can impose sanctions against a creditor who files a proof of claim, but fails to provide the documentation and information required by Rule 3001(c). Those sanctions can be evidentiary, monetary or punitive.

Proofs of claim must be signed under penalty of perjury that the statements in the claim are “true and correct and to the best of my knowledge, information and reasonable belief.” The penalty for presenting a fraudulent claim is a fine of up to $500,000 or imprisonment for up to five years, or both. The changes to Rule 3001 and the addition of Rule 3002.1 are designed to respond to cases with facts and circumstances that bankruptcy courts found to be unacceptable. The liability for attorneys and proof of claim preparers who sign inaccurate forms can be substantial.

Effective December 1, 2017: Amended Bankruptcy Rule 3007(a)(1) provides that an objection to a proof of claim and a notice of objection must be filed with the court and served at least thirty days prior to any scheduled hearing on the objection or any deadline for the claimant to request a hearing. The objection and notice must be served by first-class mail on the person designated on the original or amended proof of claim to receive notices, at the address listed for receipt of notices (except that the notice and objection must be served in accordance Rule 7004(b)(4) or (5) if the claimant is the United States and in accordance with Rule 7004(h) if the claimant is an insured depository institution).

Local courts may require claimants to request a hearing or file a response to the objection before a hearing will be scheduled or held on the objection.

In re Nations First Capital v. Decembre, BAP No. EC-19-1201-GLB (9th Circuit, Jun 05,2020) The bankruptcy court abused its discretion by reconsidering a claim disallowance under section 502(j) and FRCP 60(b)(6)) despite finding that the claimant lacked a cogent excuse for failing to respond to the claim objection. Relief under Rule 60(b)(1) based on excusable neglect was not warranted because the claimant did not overcome the presumption that mail properly addressed is presumed received by the addressee. There were no extraordinary circumstances warranting relief under Rule 60(b)(6) because the bankruptcy court had reviewed the merits of the claim when it was disallowed.

Lane v. Bank of New York Mellon (In re Lane), 18-60059 (9th Cir. June 1, 2020). Chapter 13 – mortgage lender filed to file a POC, Debtor objected “lack of standing”, lender failed to respond, default entered for debtor. Plan confirmed, discharge entered. Five years later – the bank has not pursued foreclosure. Bank wakes up to the problem and tried to set aside the order on default. Debtor believed the lien was void because the claim had been disallowed (in reality the court just determined that the creditor who filed the claim did not have standing to file the claim). BAP and 9th Circuit – opined that the finding of a lack of standing “does not imply that either the note or the lien securing the note is invalid.” That expunging the claim for lack of standing did not mean “that the note or any lien securing it was invalid or otherwise unenforceable.” and the mortgage was not void under Section 506(d) “In a nutshell, a bankruptcy court cannot destroy the property rights of the person who is the real party in interest based on the actions of a person who is not the real party in interest.”

Judge Adelman concluded the opinion by explaining how Blendheim did not control, although he said it was “superficially like this one.” The claim in Blendheim was not disallowed for lack of standing. Instead, the bankruptcy court had disallowed the claim on default based on an allegation that the claim was invalid.

In re: Los Gatos Lodge, Inc. (01/17/02 – No. 00-16916) (9th Cir. Ct App) bankruptcy trustee may not surcharge a creditor for expenses in preserving a property under 11 USC 506(c) after the secured creditor’s claim has been disallowed, even if the claim was deemed an “allowed secured claim” afterwards.

CREDITORS SHOULD FILE THEIR PROOF OF CLAIM BEFORE THE BAR DATE.

Courts Split on Allowing Late Filed POC (10/2019):

Bankruptcy Judge Michelle M. Harner of Baltimore ruled that newly modified Bankruptcy Rule 3002(c)(6) did not give her discretion to allow a creditor to file a late claim when the creditor did not know there was a bankruptcy and the creditor had been omitted from the creditor matrix. Whereas, Bankruptcy Judge Elizabeth W. Brown of Denver who reached the opposite result and found discretion to allow the filing of a late claim under the same rule.

In re Vanderpol, 19-10072 (Bankr. D. Colo. Aug. 28, 2019 – 10th Cir.) Judge Brown said she “interpreted [the rule] more broadly to apply whenever a full and complete Creditor Matrix is not timely filed, such as when a creditor is omitted from the list or is listed incorrectly in such a way that the creditor does not receive notice.” (Emphasis in original.) She went on to say that both the creditor and the debtor can benefit by a more flexible reading of the rule.

Where the benefit to the creditor is obvious, a debtor can benefit because, for example, estate assets can be paid on account of priority or nondischargeable debts.

Allowing the creditor to file a claim beyond the bar date, Judge Brown said she “believes that the intent of Congress is best effectuated by reading this rule to apply whenever the debtor fails to timely file a full and complete Creditor Matrix.”

In re Somerville, 18-20807 (Bankr. D. Md. Oct. 4, 2019, 4th Cir) If the creditor list is timely filed, Judge Harner held that “Bankruptcy Rule 3002(c)(6) does not permit enlarging the time for a moving creditor to file a proof of claim.” Although the drafters of the rule “could have intended broader coverage,” she said that she was “uncomfortable making such inferences when the language of the rule is unambiguous.”

Because the debtor had filed schedules on time, Judge Harner held that “the plain language of the Bankruptcy Rules precludes any enlargement of the claims bar date under the facts of this matter.” Nonetheless, Judge Harner said the creditor “is not without a remedy,” because the claim will not be discharged.

May 15, 2017: Resolving a split of circuits, the Supreme Court held 5/3 in Midland Funding LLC v. Johnson 6-348 (Sup. Ct. May 15, 2017) that a debt collector who files a claim that is “obviously” barred by the statute of limitations has not engaged in false, deceptive, misleading, unconscionable, or unfair conduct and thus does not violate the federal Fair Debt Collection Practices Act.

Writing the opinion for the majority in favor of the debt collector, Justice Stephen G. Breyer said that the conclusion on one issue — false, deceptive or misleading — was “reasonably clear.” The second issue — unfair or unconscionable — presented a “closer question,” he said. The dissent replied that “Professional debt collectors have built a business out of buying stale debt, filing claims in bankruptcy proceedings to collect it, and hoping that no one notices that the debt is too old to be enforced by the courts. This practice is both ‘unfair’ and ‘unconscionable.’”

The majority of the Court did not rule that the later adoption of the Bankruptcy Code implicitly repealed aspects of the FDCPA. However, the opinion opens the door for debt collectors to purchase time-barred claims for pennies on the dollar and profit by filing those otherwise uncollectable claims, because trustees and debtors will not always object.

(History of Midland: In an action under the Fair Debt Collection Practices Act, 15 U.S.C. sections 1692e and 1692f, arising out of a Chapter 13 bankruptcy case in which a creditor filed a claim asserting that debtor owed a credit-card debt and noting that the last time any charge appeared on debtor’s account was more than 10 years ago, which exceeded the 6-year statute of limitations, the Eleventh Circuit Court of Appeals’ decision that the FDCPA applied to the case is reversed in Midland where the filing of a proof of claim that is obviously time barred is not a false, deceptive, misleading, unfair, or unconscionable debt collection practice within the meaning of the Fair Debt Collection Practices Act.)

In re Barker, 9th Cir Ct Appeals, referral from 9th BAP 10/2016. re late filed POC – Agreeing with the Seventh Circuit, the panel held that if a creditor wishes to participate in the distribution of a debtor’s assets under a Chapter 13 plan, it must file a timely proof of claim under Federal Rule of Bankruptcy Procedure 3002. The debtor’s acknowledgment of debt owed to the creditor in a bankruptcy schedule does not relieve the creditor of this affirmative duty.

Eleventh Circuit holds that filing a proof of claim in bankruptcy on a time-barred debt violates the FDCPA. In Crawford v. LVNV Funding, LLC, the Eleventh Circuit became the first federal circuit court of appeals to hold that filing a proof of claim on a time-barred debt in a bankruptcy case violates the Fair Debt Collection Practices Act (“FDCPA”).[1] See No. 13-12389,__ F.3d __, 2014 WL 3361226 (11th Cir. July 10, 2014). The case arose when LVNV filed a proof of claim in Crawford’s bankruptcy case on a debt for which the statute of limitations had expired. In response, Crawford filed an adversary proceeding against LVNV, alleging that LVNV routinely filed proofs of claim on time-barred debts and that LVNV’s actions violated the FDCPA.

The Court concluded that “a debt collector’s filing of a time-barred proof of claim creates the misleading impression to the debtor that the debt collector can legally enforce the debt.” Id. at 4. The “least sophisticated consumer” may therefore fail to object to the claim, and, due to the Bankruptcy Code’s automatic allowance provision, the claim will be paid out of the debtor’s wages. For these reasons, the court found that filing a proof of claim on a time-barred debt was unfair, unconscionable, deceptive, and misleading, in violation of §§ 1692e and 1692f of the FDCPA.

In re Maui Indus. Loan & Fin. Co., Case No. 10-00235, 2017 Bankr. LEXIS 2553 (Bankr Ct, D. of Hawaii, September 7, 2017) ISSUE: Whether, in a Ponzi scheme case, the timely-filed claims of investors for lost profits should be paid before or after the untimely-filed claims of investors for lost principal. HOLDINGS: [1]-Timely filed claims must be paid first, including lost profits portion of timely claims filed in a case involving a Ponzi scheme; [2]-Where one of the tardy claims arose because the claimant did not have notice of the bankruptcy filing, 11 U.S.C.S. § 726(a)(2)(C) applied and the claim was treated as timely; [3]-With respect to the untimely claims seeking to recoup lost principal, they had to be paid after the timely claims, including those for lost investment profits, because the timely lost profits claims were “deemed allowed” given a lack of any objection, and the court could not use its equitable powers to override the clearly stated priority order in the Code.

Decision: Court ordered that all timely claims be paid first.

In re Barker, 9th Cir. Ct Appeals, BAP No. 13-1393, 10/27/16 The panel affirmed the Bankruptcy Appellate Panel’s affirmance of the bankruptcy court’s decision to disallow a creditor’s late-filed claims in a Chapter 13 proceeding.

Agreeing with the Seventh Circuit, the panel held that if a creditor wishes to participate in the distribution of a debtor’s assets under a Chapter 13 plan, it must file a timely proof of claim under Federal Rule of Bankruptcy Procedure 3002. The debtor’s acknowledgment of debt owed to the creditor in a bankruptcy schedule does not relieve the creditor of this affirmative duty.

In re Washington, BAP NO. CC-18-1206-LKuF (July 30, 2019 Debtor Gwendolyn Washington obtained a chapter 7 discharge, which extinguished her personal liability on the debt secured by a junior lien on her residence. About five years later, she filed a chapter 13 case; she obtained an order valuing at zero the junior lien held by Option One Mortgage Corporation, serviced by Real Time Resolutions, Inc. (“RTR”). RTR filed an unsecured claim in the full amount of the debt it believed it was owed; Ms. Washington objected on the ground that her personal liability had been discharged. The bankruptcy court overruled the objection, concluding that the discharge did not fully eliminate the claim and that the plain language of § 506(a) required the allowance of RTR’s unsecured claim in the amount of $307,049.79. We REVERSE.

CONCLUSION: post-confirmation claim objections to secured claims are barred by res judicata, while post-confirmation claim objections to unsecured claims are not barred by res judicata.

In re Anna Stahl, 9th Cir BAP, CC-20-1254-SGF (Apr 07,2021)The bankruptcy court did not abuse its discretion by relying exclusively on the schedules to calculate chapter 13 Debtor’s eligibility. The BAP also rejected Appellant’s argument that the bankruptcy court was bound to include the stated amount of its proof of claim in determining Debtor’s chapter 13 eligibility because Debtor did not object to its claim.

The changes also require an ongoing requirement for claimants in Chapter 13 cases. Creditors in Chapter 13 cases whose claims are secured by a security interest in a debtor’s principal residence and whose claims are for arrearages being cured through a Chapter 13 plan, are required to file a Notice of Payment Change (Official Form B10, Supplement 1) no later than 21 days before the new amount is due. This consists of a change in the mortgage payment amount, including those changes which arise from escrow adjustments or from interest rate changes. The Notice of Payment Change must be served upon the debtor, the debtor’s counsel and the Chapter 13 trustee. The Notice of Payment Change must be filed as a proof of claim supplement in the proof of claims registry.

The consequences for the mortgage creditor who fails to file a timely Notice of Payment Change will render the payment change ineffective. Mortgage creditors who fail to comply can expect evidentiary sanctions, where the court can prohibit a creditor from presenting evidence in a dispute about the claim. The court also has discretion to “award appropriate relief, including reasonable expenses and attorneys’ fees”.

Mortgage creditors in Chapter 13 cases whose claims are secured by a security interest in a debtor’s principal residence and whose claims are being paid through a Chapter 13 plan, are required to file a Notice of Fees, Expenses and Charges (Official Form B10, Supplement 2) every 180 days (the “Notice of Fees”) while the Chapter 13 case is ongoing. The Notice of Fees must be filed as a supplement to the mortgage creditor’s proof of claim in the bankruptcy court’s claims registry, and it must be served on the debtor, the debtor’s attorney and the Chapter 13 trustee within 180 days of when the charges were incurred. Failure to timely file the Notice of Fees will result in the inability for the creditor to collect the fees and expenses which should have been disclosed in the Notice of Fees.

Fees, expenses and charges include late fees, attorneys’ fees, inspection fees, taxes advanced, property preservation fees and forced place insurance. The trustee and/or the debtor have up to one year after the filing of the Notice of Fees to file a motion requesting a hearing on whether or not the payment of the fees and charges in the Notice of Fees are lawful.

Pursuant to Rule 3002.1(f) – (h), within 30 days after a debtor completes all Chapter 13 plan payments, the trustee must file and serve a notice stating the debtor has paid in full the amount required to cure the default on the creditor’s claim (the “Final Cure Notice”). The Final Cure Notice must include a statement that advises mortgage creditors of their obligation to file a response within 21 days after the Final Cure Notice. Failure to file the written response within this time period may be fatal to the creditor’s position.

The mortgage creditor’s response must state: (1) whether it agrees with the assertion that the debtor has paid the amount needed to cure the default on the creditor’s claim; (2) whether the debtor is otherwise current; or (3) if the creditor asserts the debtor has not cured the default, the creditor must provide an itemization of the cure amount. The mortgage creditor’s required response also must be filed as a supplement to the mortgage creditor’s proof of claim in the claims registry, in addition to being served on the debtor, debtor’s attorney and the Chapter 13 trustee.

In 9th Circuit, no postpetition interest on unsecured claims.

The Code’s clear language. The Code prohibits claims for postpetition interest on unsecured claims. 11 U.S.C. §§ 502(b)(2), 506(b). In re Del Mission Ltd., 998 F. 2d 756, 757 (9th Cir, 1993).

In 9th Circuit, interest accrues on postpetition nondischargeable debts.

In the Ninth Circuit as well, interest continues to accrue postpetition on nondischargeable debts. In re Hamilton, 584 BR 310 (BAP 9th Cir 2019), affirmed by the Ninth Circuit (11/21/2019, 18-60026, 18-60027), citing In re Shoen, 176 F.3d 1150, 1166 (9th Cir. 1999) (per curiam).

In Hamilton affirmed by the Ninth Circuit, the BAP cited the Supreme Court’s Bruning case, which dealt with nondischargable tax debt, and found the same rationale should apply to interest on a nondischargable judgment debt under § 523(a)(6). “In most situations, interest is considered to be the cost of the use of the amounts owing a creditor and an incentive to prompt repayment and, thus, an integral part of a continuing debt. Interest on a tax debt would seem to fit that description.” Hamilton, 584 BR at322, citing Bruning, 376 U.S. at360.

In 9th Circuit, no interest on mortgage debts.

Also in the 9th Circuit, there’s no interest on mortgage arrearages. In re Laguna, 944 F.2d 542 (9th Cir, 1991), citing interplay between 1322(b) and 1325(a), and following the Fourth Circuit in Landmark Fin. Servs. v. Hall, 918 F.2d 1150 (4th Cir.1990).

MERTOLA, LLC, v. SANTOS, No. 1 CA-CV 16-0168 (AZ Court of Appeals, Division 1,Decided: March 02, 2017) We hold in this case that, absent agreement to the contrary, a cardholder’s failure to make a minimum monthly credit-card payment does not trigger the statute of limitations on a claim for the entire unpaid balance on the account. Absent contrary terms in the account agreement, the lender’s claim for the balance does not accrue, and limitations does not begin to run, until the lender accelerates the debt or otherwise demands payment in full.

In In re Woodbridge Grp. of Companies, LLC, No. BR 17-12560-BLS, 2019 WL 4305444 (D. Del. Sept. 11, 2019), the United States District Court for the District of Delaware affirmed an opinion by Bankruptcy Judge Kevin Carey, and held that a proof of claim will be expunged if the note and loan agreement underlying the claim prohibit assignment and provide that assignment without consent will be “null and void.” Read more…

Mastan v. Salamon (In re Salamon) (4/20/17) The Ninth Circuit affirmed the BAP, concluding that the junior creditor lost its right to convert its nonrecourse claim to a recourse claim under section 1111(b) of the Bankruptcy Code as a result of the senior creditor’s sale of the collateral. Section 1111(b) requires a nonrecourse claim “secured by a lien on property of the estate” to be treated as recourse “whether or not [the creditor] had recourse against the debtor on account of such claim.”

In Re J.H. Investment Services, Inc., (11/22/11 – Ct of Appeals 11th Cir) held that the IRS had waived its right to an unsecured deficiency by filing a proof of claim that evidenced a secured claim but failed to note that a portion of the claim may be unsecured. The court held that the latter set of rights, plan voting and distribution towards the unsecured portion of an otherwise secured claim, could be waived if not pursued through express reference in a proof of claim.

Can a debtor file a proof of claim for the creditors? Yes, the debtor may file a claim for a creditor up to 30 days after the claims bar date. See BR 3004.

Question: Creditor (second mortgage) cancels debt several years ago and issues a 1099. Debtor takes the tax hit. Debtor now in a ch. 13 to address the first mortgage. Creditor who cancelled mortgage just filed a claim. Can a creditor claim it is owed money by filing a POC?

Answer?: According to IRS a 1099-C is just a required form so creditor can take loss but does not bar collection down the road (presumably would have to adjust the declared tax loss later if collected). Of course, this happens all the time in debt buying scenario. Most credit card debts are “charged off” and 1099-C may be issued then sold to debt buyer who collects from consumer down the road.

in chapter 13 cases there is a split of authority and fact dependent. For example, here is an interesting case to start with which (in my cursory review) held mortgage creditor could file/collect POC on principle (stating that as the minority view) but not (some) interest, collection costs, or attorneys’ fees alleged to be due: In re Reed, 492 B.R. 261, 273 (Bankr. E.D. Tenn. 2013).

SHORT SALES (law may be dictated by each state or federal): In some circumstances, ORS 86.157(2) will create a bar against an action for residual debt after a short sale: “If a lender reports to the Internal Revenue Service that as a consequence of or in conjunction with a short sale of residential property the lender has canceled all or a portion of a borrower’s obligation under a real estate loan agreement and the lender provides to the borrower written evidence of the lender’s report to the Internal Revenue Service, the lender or an assignee of the lender may not bring an action or otherwise seek payment for the residual debt following the short sale.” (Some terms are defined in the statute.)

1.4 million in late fees is unconscionable, illegal or otherwise against public policy.

Dobson Bay Club II DD, LLC v. La Sonrisa de Siena, LLC, 242 Ariz. 108 (2017), 393 P.3d 449, 763 Ariz. Adv. Rep. 19 Nearly $1.4 million late fee assessed on final loan balloon payment for $28.6 million commercial loan constituted an unreasonable and unenforceable penalty, rather than a valid provision for liquidated damages; in addition to late fee, borrower had obligation under terms of note to pay regular and default interest, collection costs, trustee’s fees and costs and attorney fees as a consequence of six-month delay in paying the balloon, flat 5% late fee on did not reasonably predict the damages that would be sustained by lender for a late balloon payment of the entire loan principal, nothing in record indicated the lender or its successor in interest suffered an uncompensated loss that approached $1.4 million, and the difficulty of proving loss as identified in the late fee provision was slight. Restatement (Second) of Contracts § 356(1)

“A liquidated damages contract provision is enforceable if the pre-determined amount for damages seeks to compensate the non-breaching party rather than penalize the breaching party. We here hold that a nearly $1.4 million late fee assessed on a final loan balloon payment constitutes an unenforceable penalty.”

In re MATTHEW BORRE, Debtor, Case No. 17-24543-E-13, 03-01-2019 Question – the “grace period” is between date mortgage due and date payment deemed in default. In this case the borrower/debtor paid before the end of the grace period, but lender filed POC showing the in default for the same amount collected during the grace period. Judge found the POC is profferred under penalty of perjury. The signatory certifies that the creditor gave the debt credit for any payment receive on the debt. In this case the lender’s POC was incorrect (the debtor had not received credit for the payment made during the grace period). The court found that filing a proof of claim is not merely a series of allegations based on information and belief, which if true, might support the relief requested (such as when filing a complaint). The filing of a proof of claim is much more significant and the statements therein are provided with, and subject to, higher standards. Court awards attorneys fees to debtor given the creditor’s prolonged proceedings.